President Donald Trump and his guests at the Rose Garden today celebrated Liberation Day. Stock investors won't be celebrating tomorrow based on the plunge in futures prices tied to the DJIA, S&P 500, and the Nasdaq-100. The Stock Market Vigilantes are not happy.

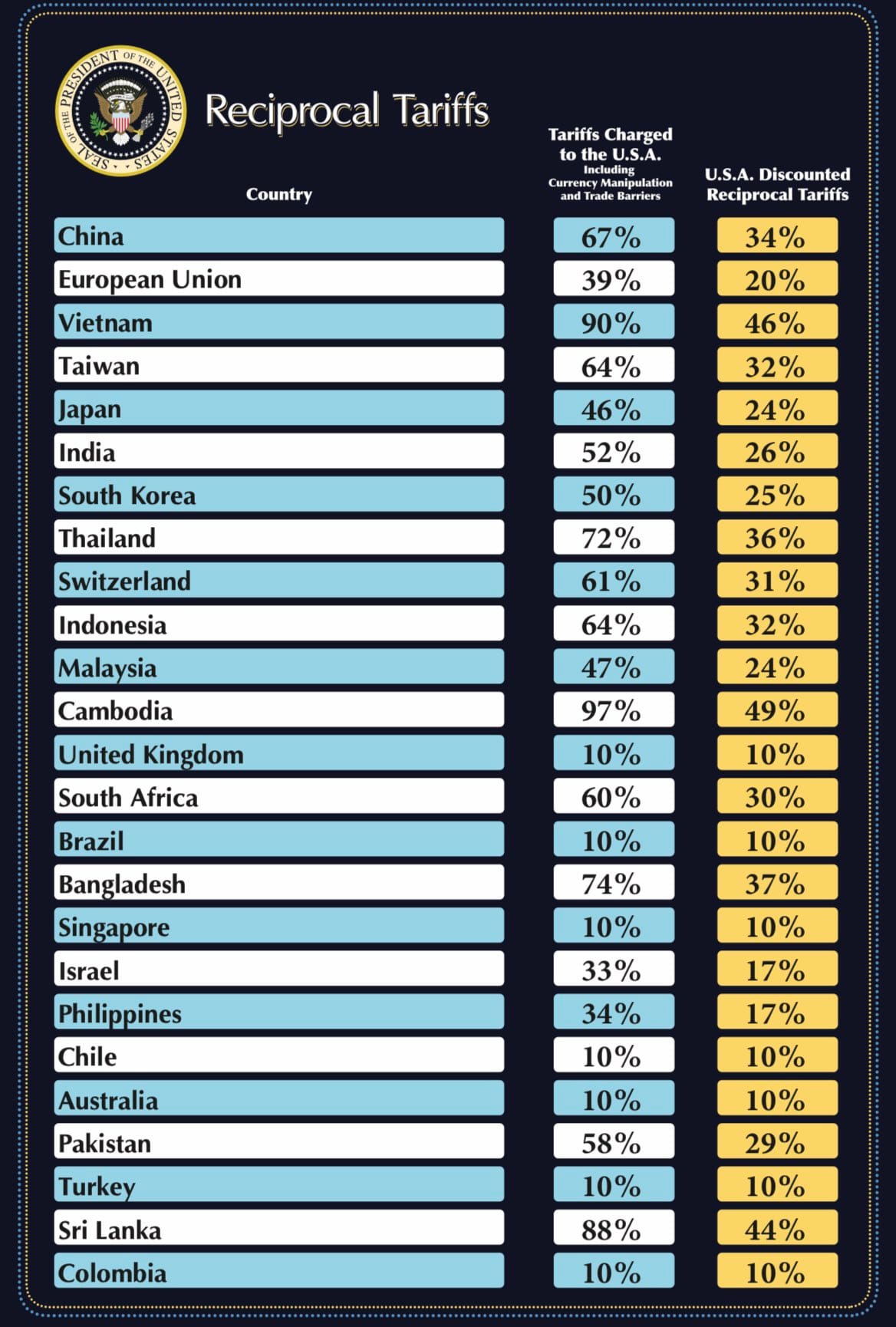

Trump announced that on April 5, his administration will impose a 10% tariff rate on all imports from all of America's trading partners. The 60 "worst offenders," which are countries deemed to have onerous nontariff barriers to their markets, will have their own reciprocal tariff rates starting on April 9. Trump's Reign of Tariffs exceeds most expectations. The day after Liberation Day may be more like D-Day on Wall Street. That's too bad.

President Trump said that the tariffs charged by the US will be lower than the effective rates (including nontariff barriers and currency manipulation) charged to the US (table). (A more comprehensive list is included in a thread on X.) He is willing to negotiate reciprocal reductions in tariffs. However, 25% permanent tariff rates will still apply to autos, steel, and aluminum.

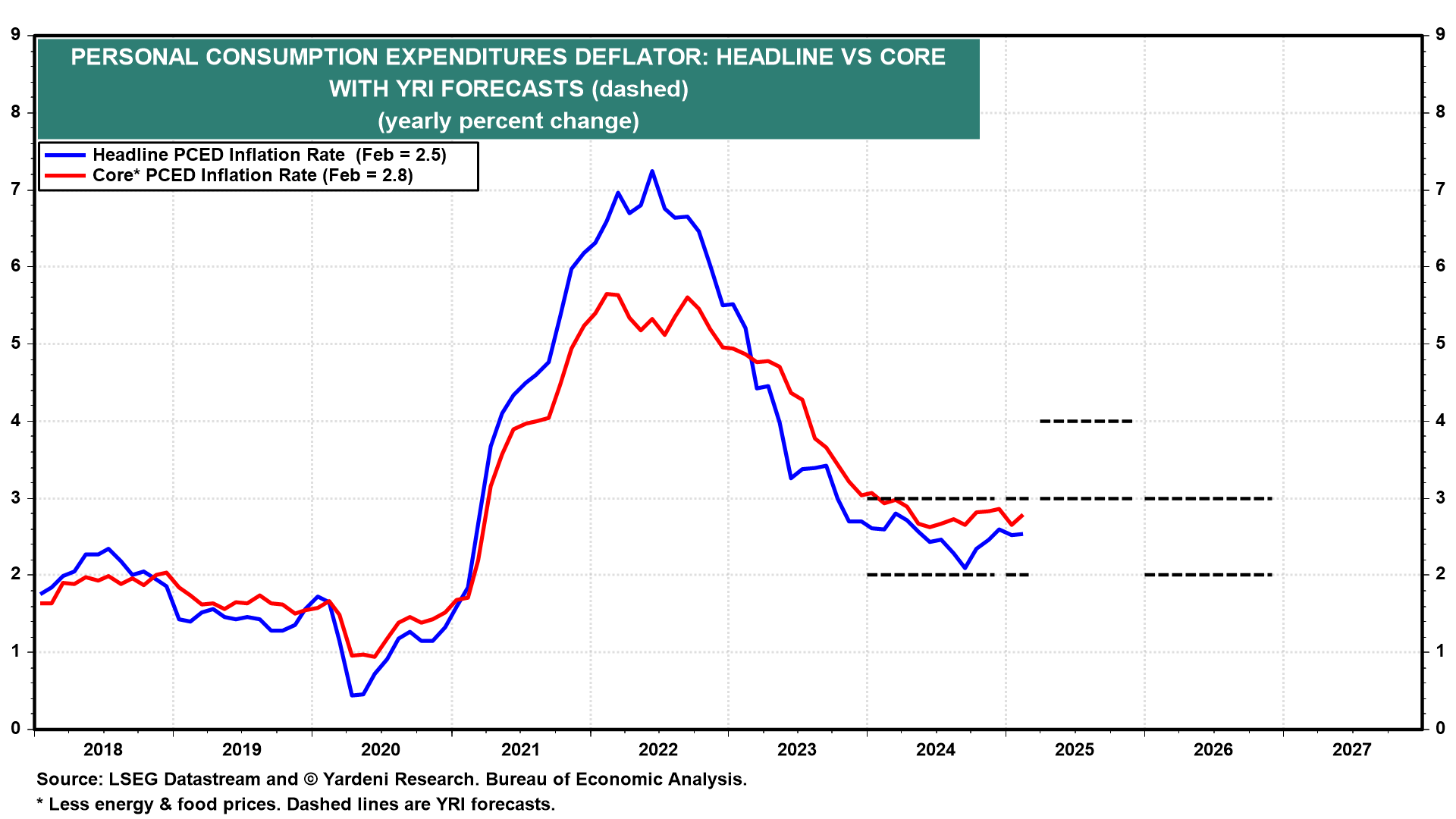

We've recently warned that Trump's Reign of Tariffs is very likely to boost inflation over the rest of the year, depressing overall consumer sentiment, real wages, and consumer spending. Rising goods prices could boost the PCED inflation rate from 2.0%-3.0% currently to 3.0%-4.0% over the rest of this year (chart). If the result is a consumer-led slowdown later this year (after a short auto-buying binge), the Fed won't be able to help by easing monetary policy if inflation remains well above its 2.0% target. The result could be 6-12 months of stagflation.

The economy won't get a boost this summer from fiscal policy if the Republicans manage only to extend the 2017 tax cuts already in place. If they fail to do so, the result would be a tax increase, which could cause a recession. The odds of the Republicans’ losing their majorities in both houses of Congress are increasing.

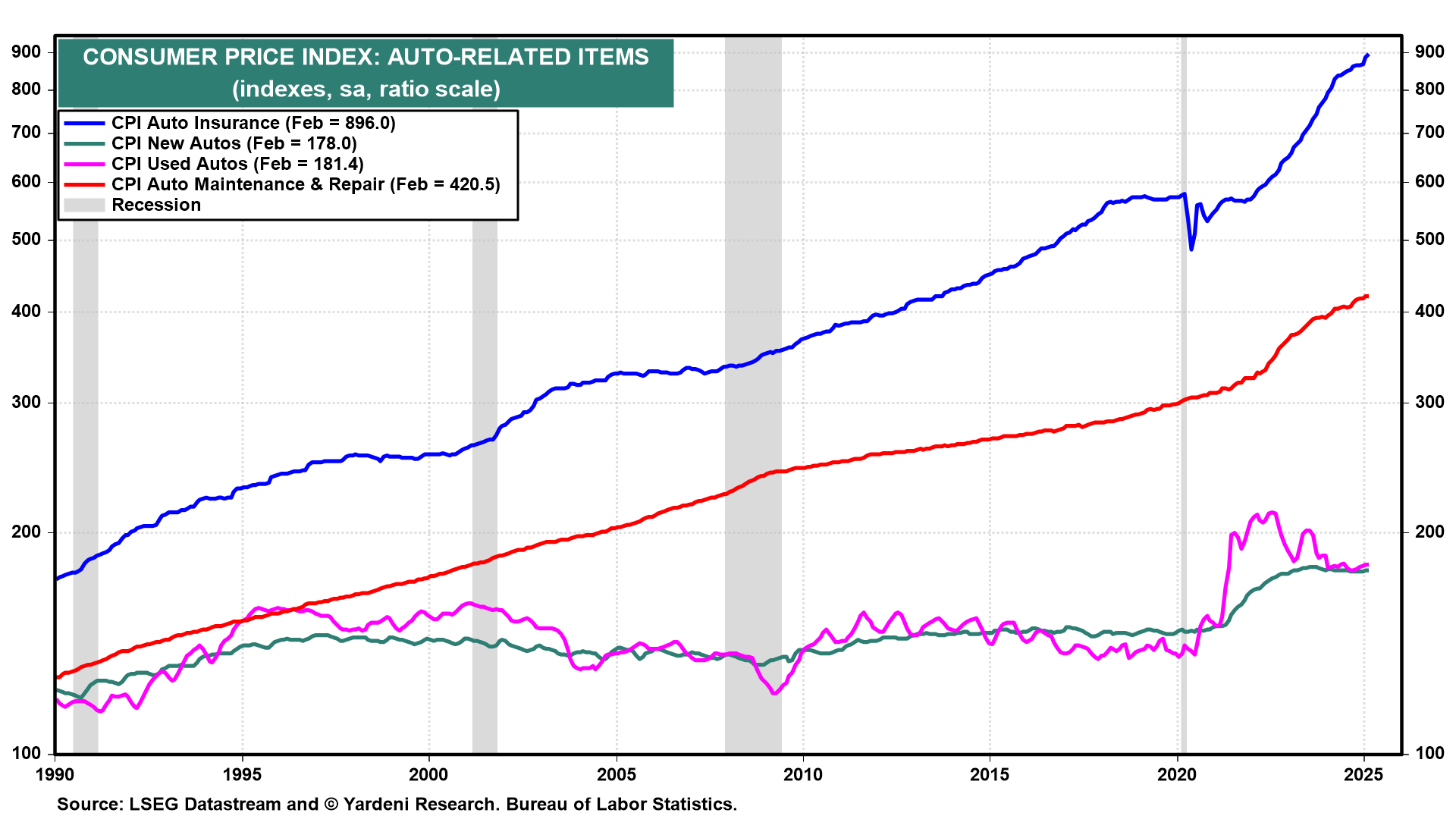

The 25% tariffs on autos, auto parts, steel, and aluminum undoubtedly will boost new as well as used auto prices as well as auto insurance, maintenance, and repair costs. That could lead to persistent inflationary pressures in the broader economy, mirroring what happened during the pandemic (chart).

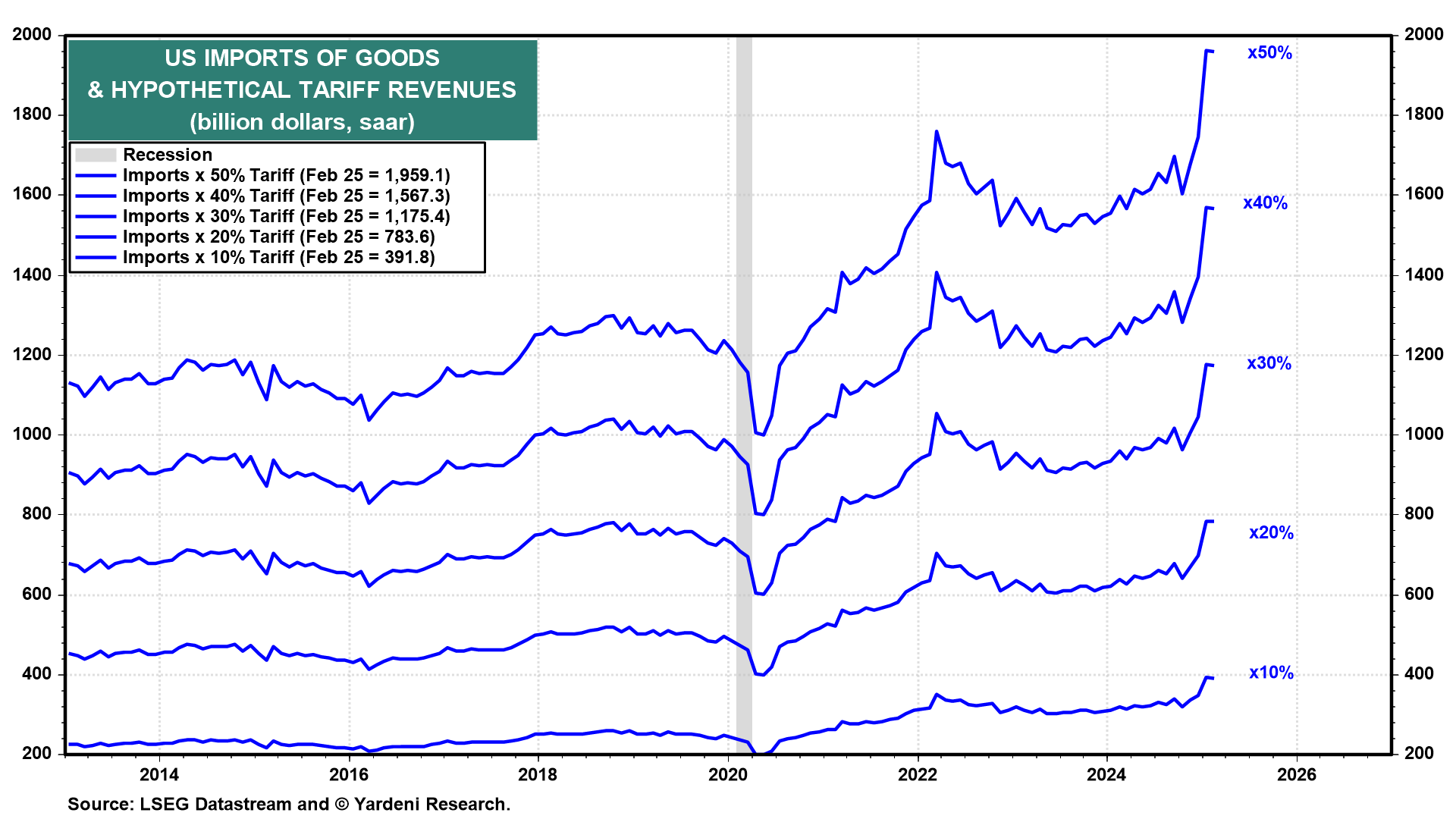

We hope that many of the reciprocal tariff rates will be negotiated down throughout the year. We expect that the 10% tariff floor plus some additional tariffs on key countries like China will still exist by year-end. That suggests at least $300 billion in annual tariff revenues, or maybe $600 billion if the average rate is closer to 20% (chart). That will dent the federal budget deficit, but will remain below the government’s net interest payments, which will likely exceed $1 trillion this year.

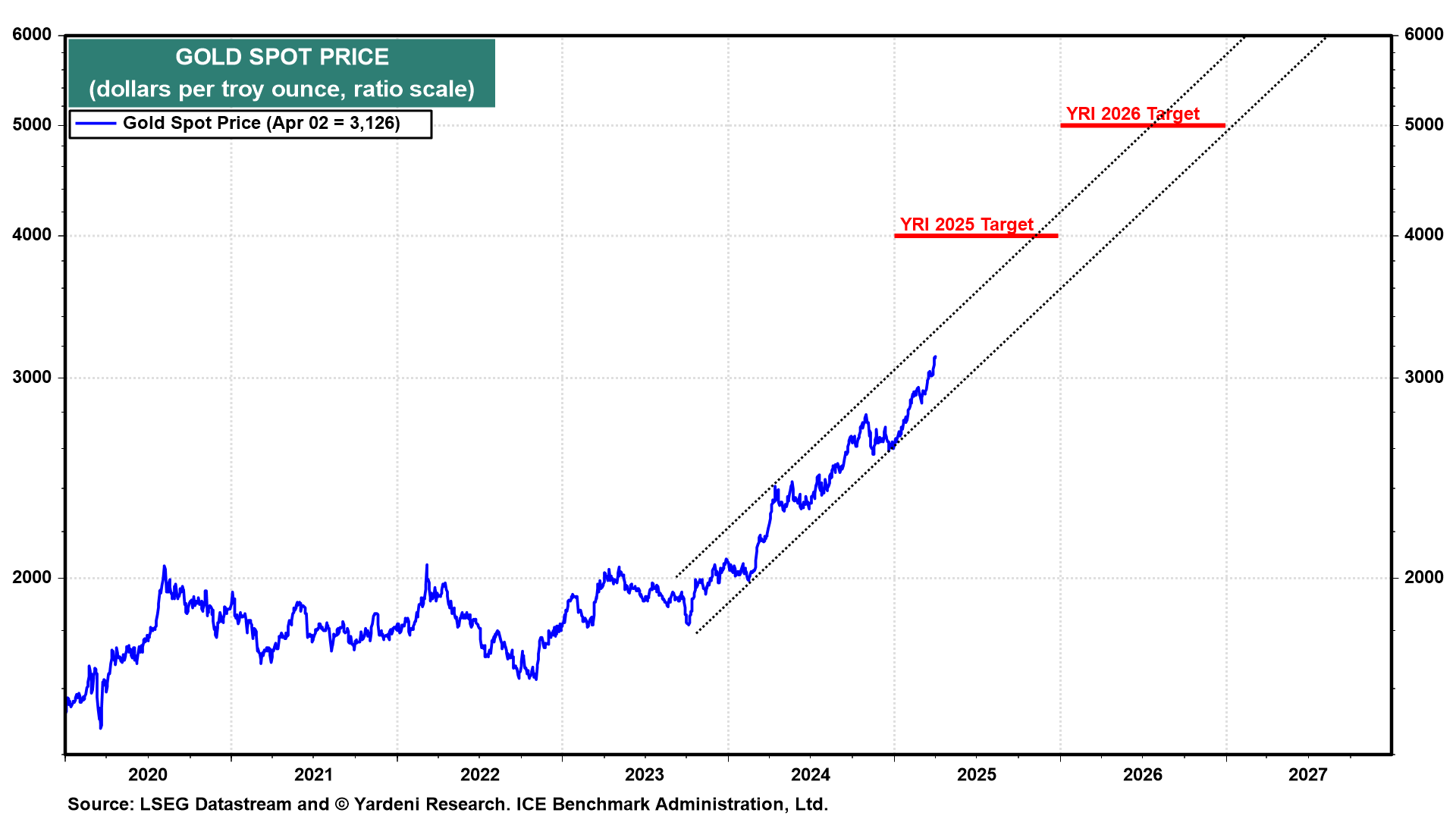

The nearby futures price of gold surged to a new record high of $3,192 per ounce in response to Trump's announcement. We expect the gold price to reach $4,000 by the end of the year (chart). That may happen sooner if Trump persists with his Reign of Tariffs.