The stock market sold off this morning on a decline in February's Consumer Confidence Index (CCI), confirming a similar decline in February's Consumer Sentiment Index (CSI), which was reported at the end of last week. The CSI survey tends to be more affected by inflation, while the CCI survey is more affected by employment. The former was weak this month on concerns about rising inflation, while the latter was weak mostly on expectations of fewer job openings in six months. Both are very volatile on a monthly basis. Both may be reflecting extreme partisanship, with Democrats much less confident than Republicans, in our opinion. Let's review the CCI data in 10 charts:

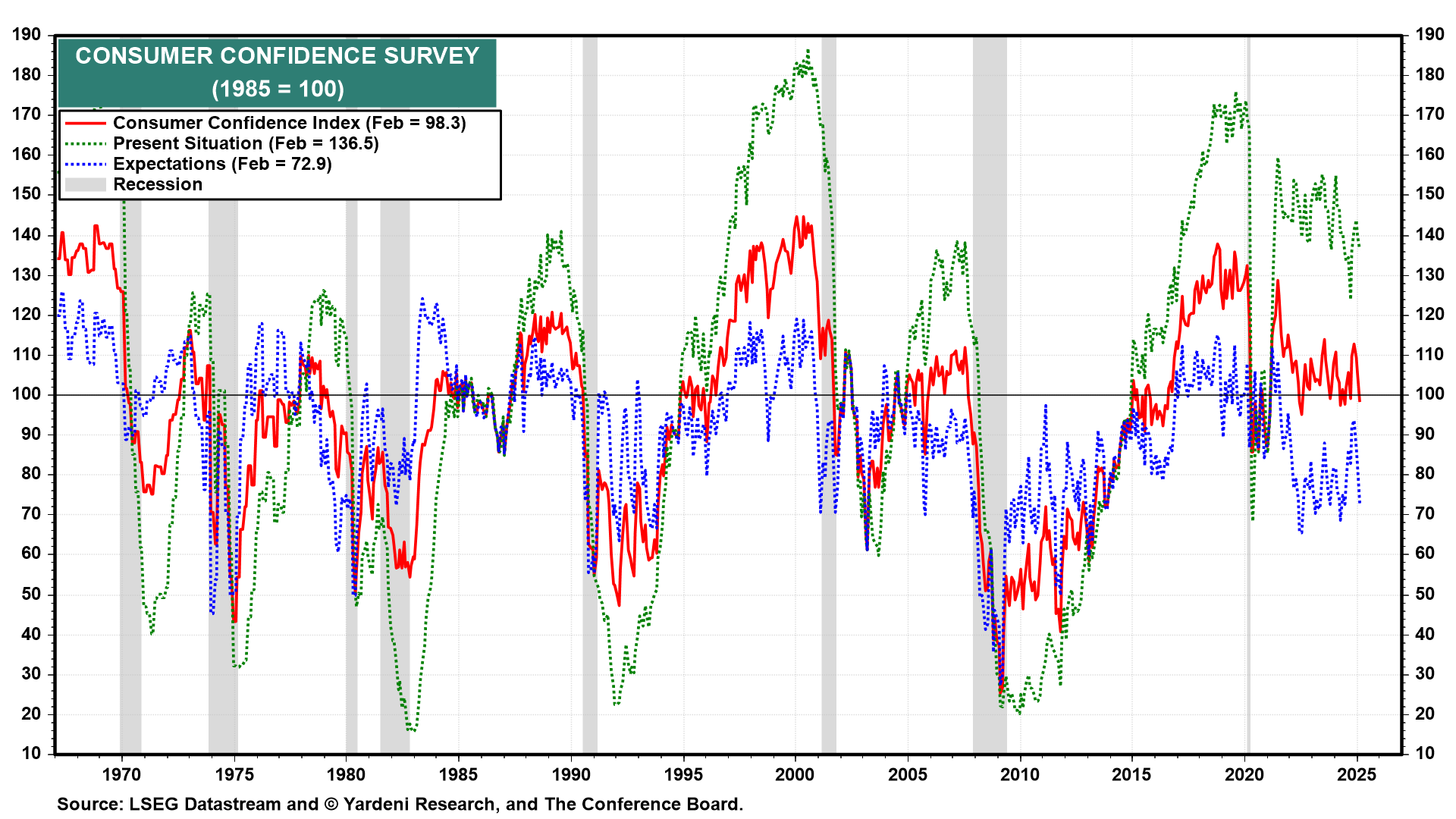

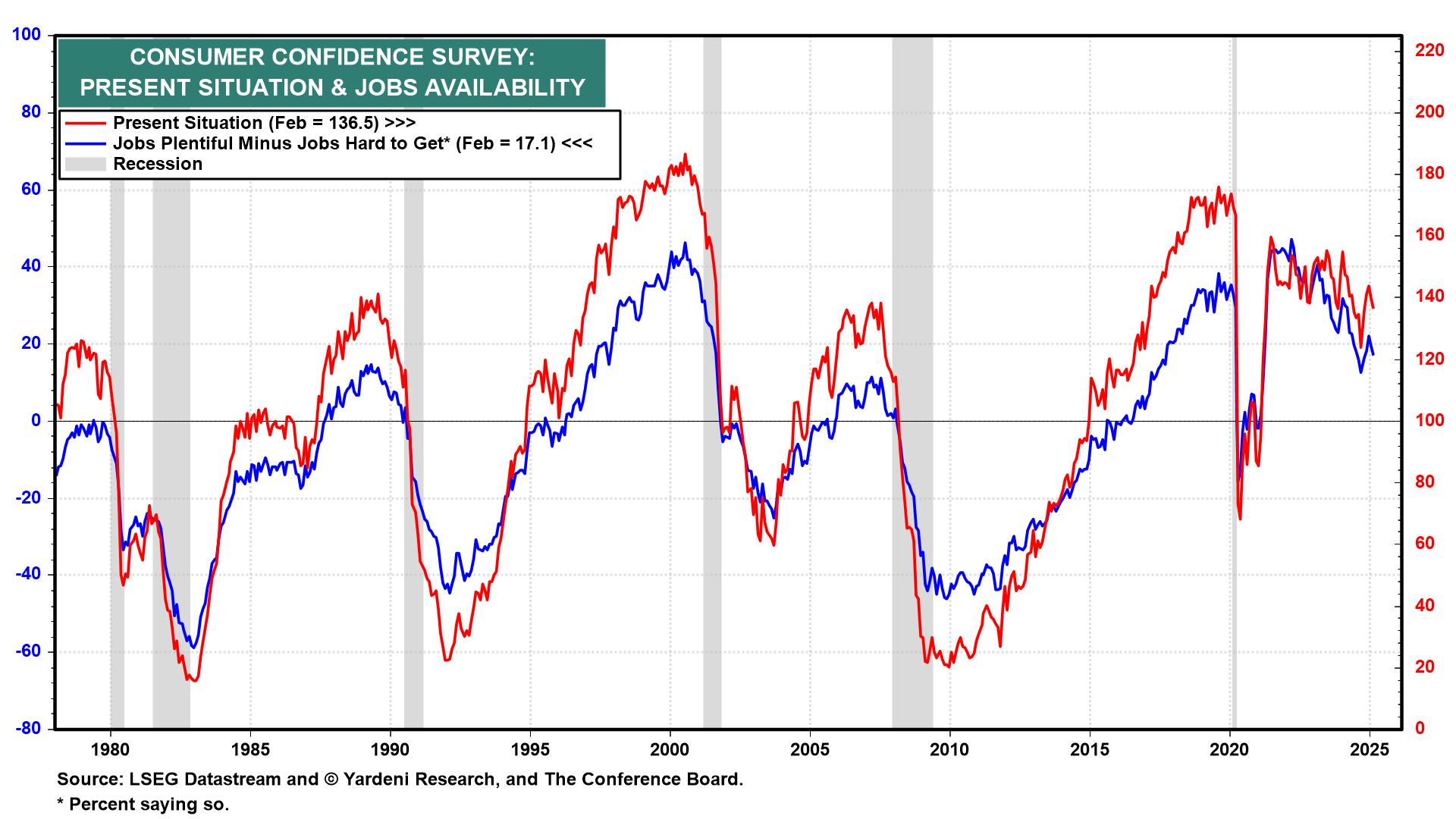

(1) In February, there was a big drop in the expectations component of the CCI. The present situation component of the CCI dipped but remained relatively high. We think that the present situation component is a better indicator of the economy's current performance than is the expectations component, which is more volatile as well.

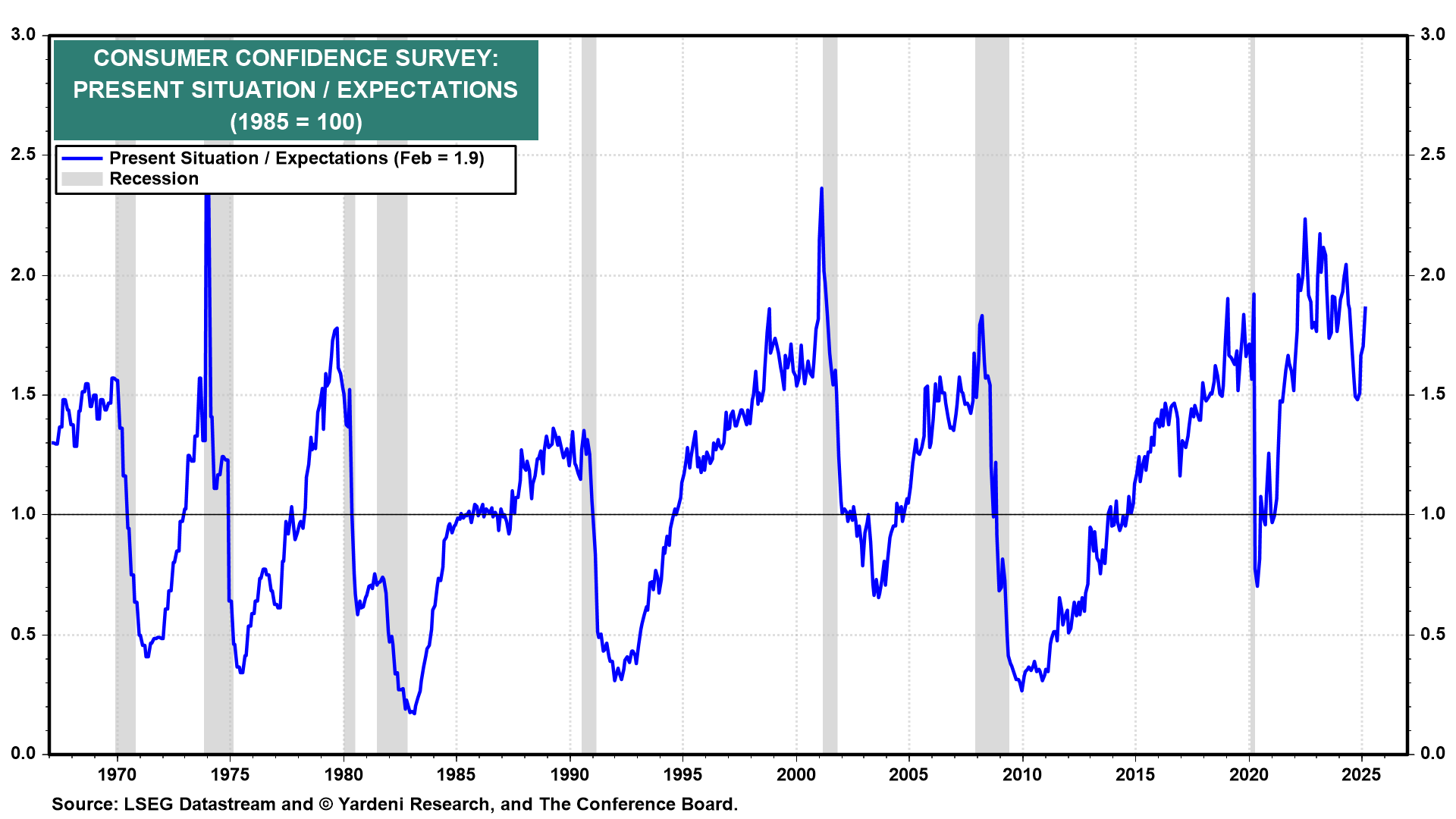

(2) The ratio of the present situation and expectations components of the CCI rose this month and remains relatively upbeat given that the former tends to exceed the latter.

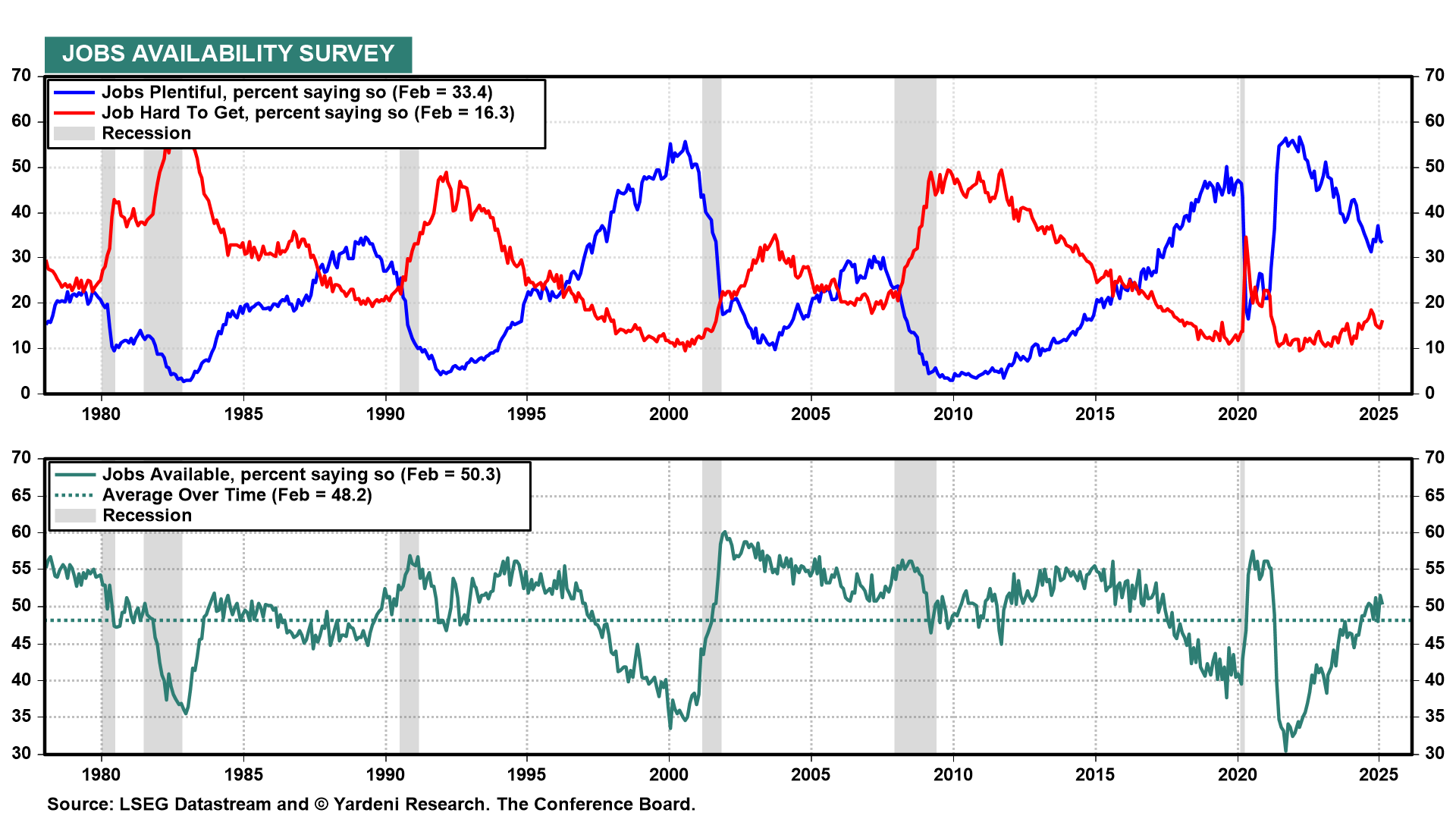

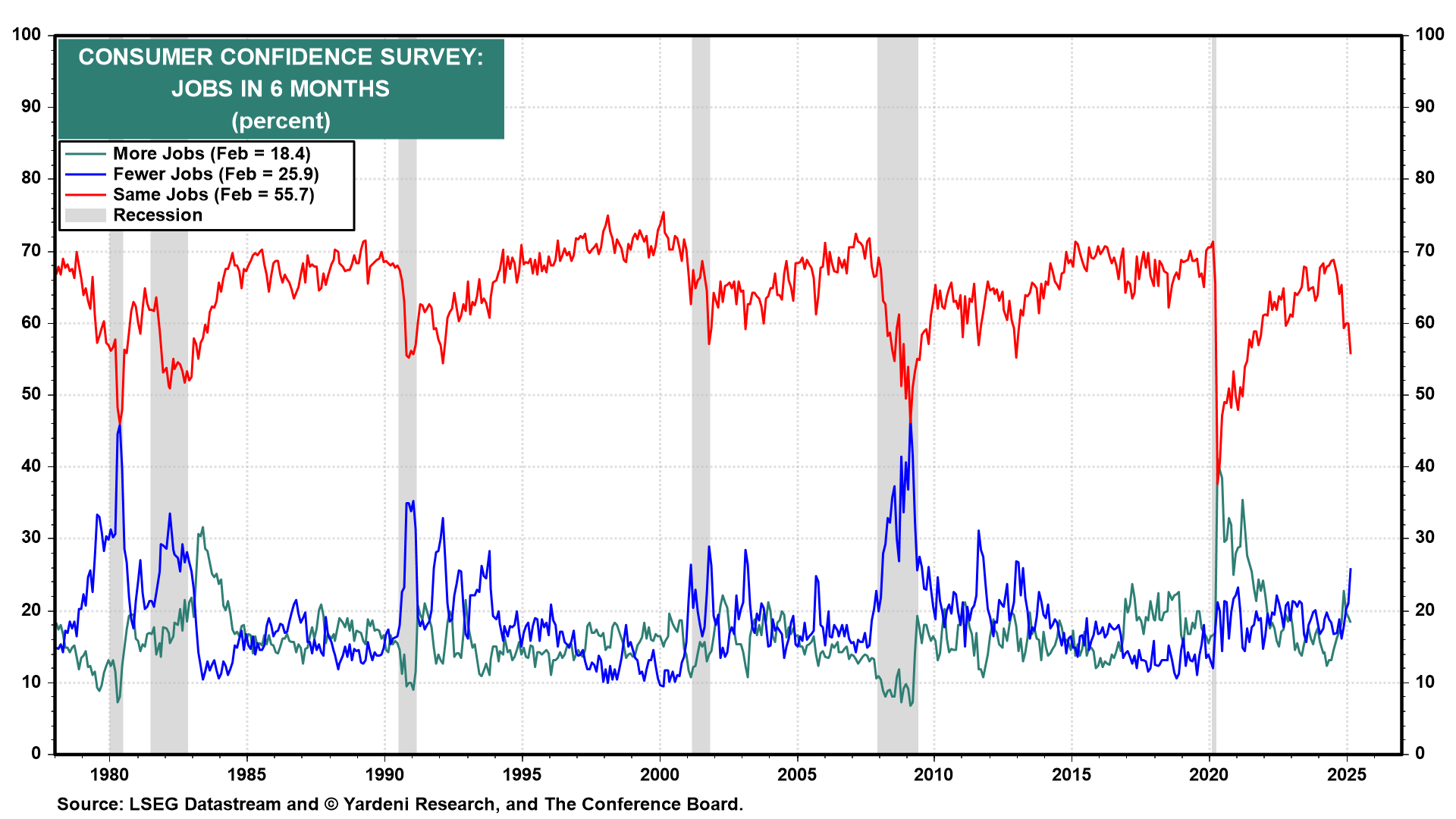

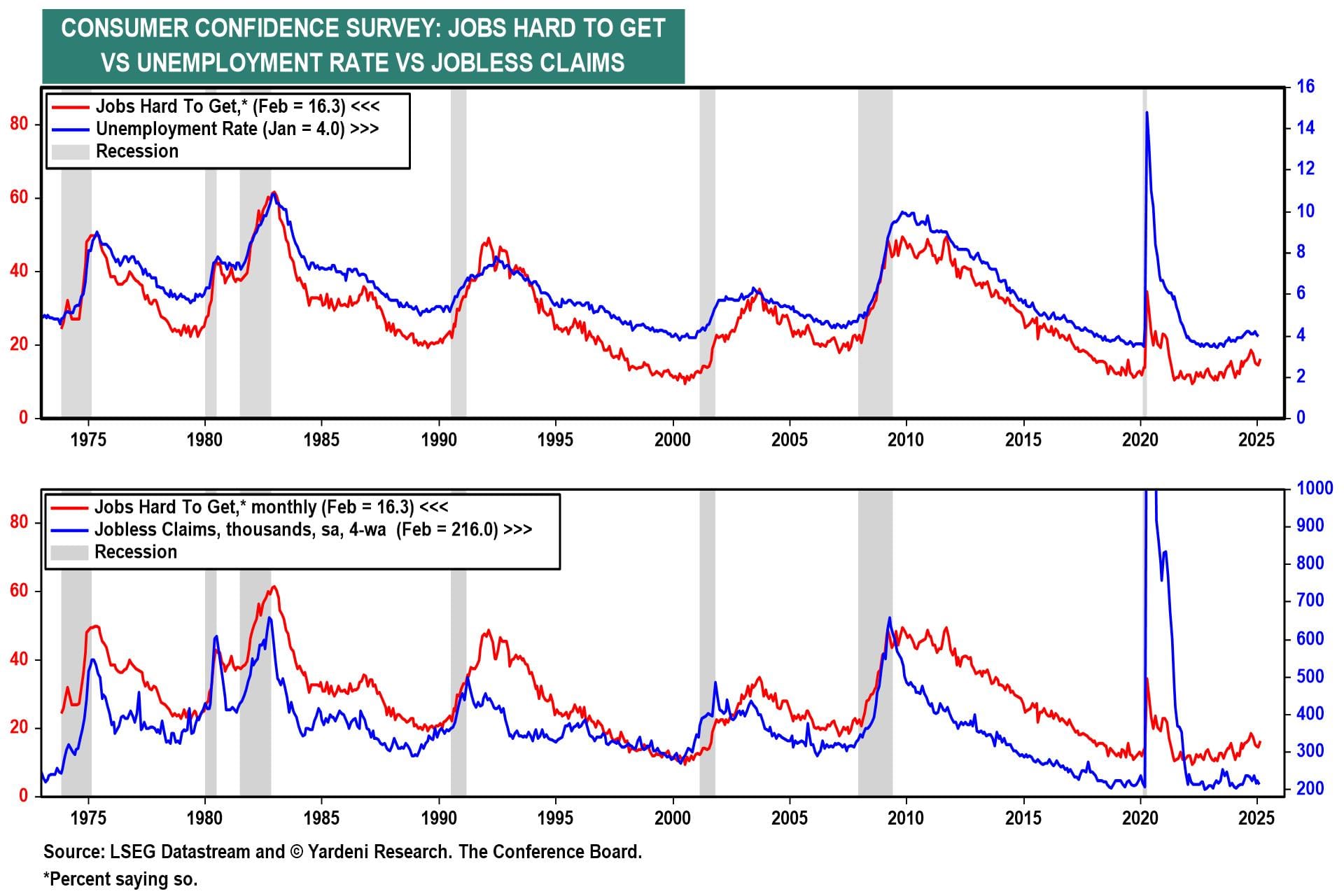

(3) Jobs are mostly available (with 50.3% of respondents saying so). The jobs-plentiful response remains relatively high (at 33.4%). The jobs-hard-to-get response edged up to 16.3%, which is a relatively low reading.

(4) The CCI present situation component is highly correlated with jobs-plentiful minus jobs-hard-to-get series. The current readings of both series are consistent with a solid labor market.

(5) The drop in the CCI expectations component reflects the decline in the "same number of jobs in 6 months" response from 68.8% during July 2024 to 55.7% currently. The "fewer jobs in 6 months" response jumped from 21.0% in January to 25.9% in February. This may reflect all the news about federal job reductions under Trump 2.0.

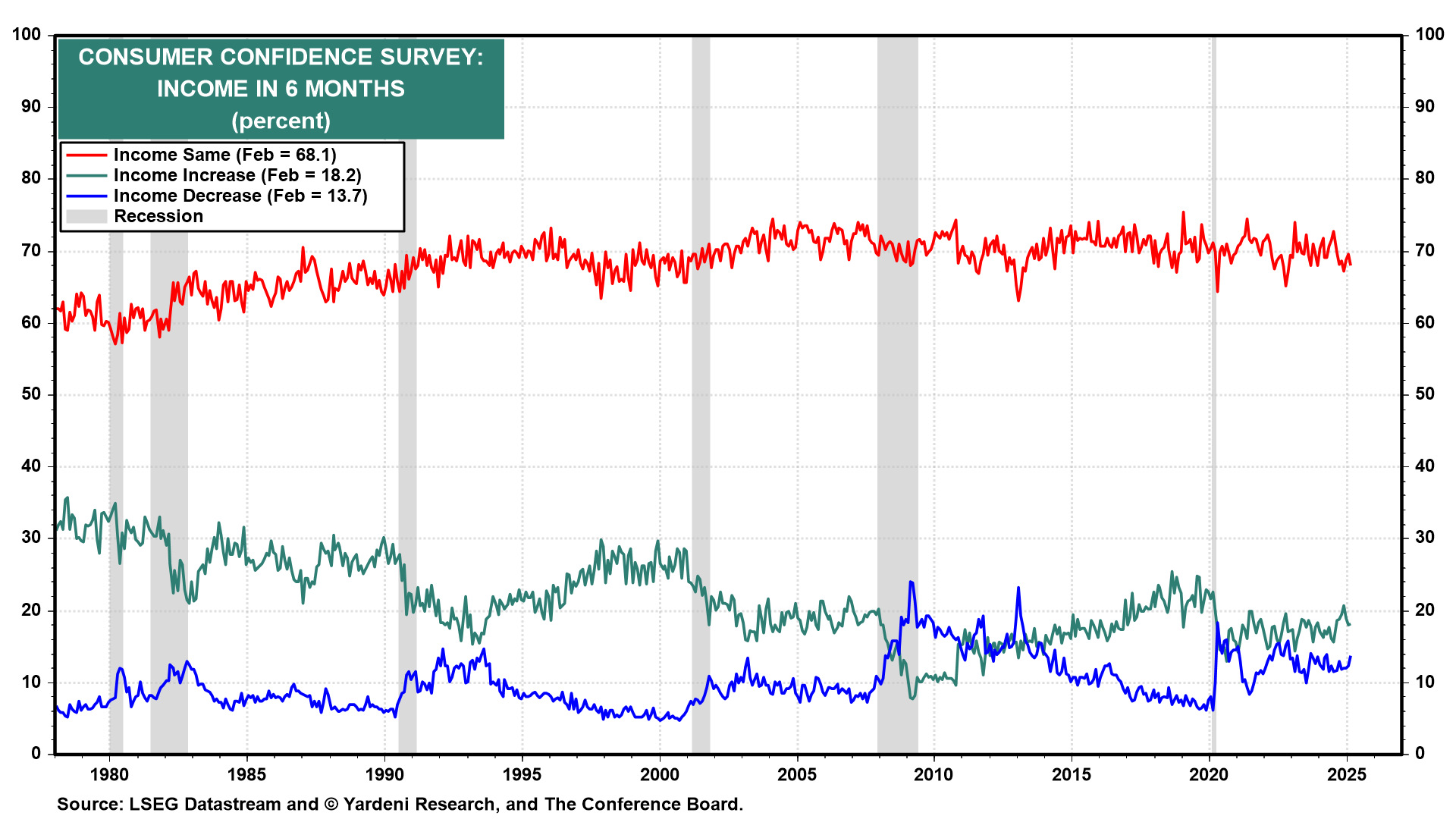

(6) The outlook for incomes in six months hasn't changed very much in recent years, with 68.1% currently expecting the same income. In addition, 18.2% expect increases, while 13.7% expect decreases.

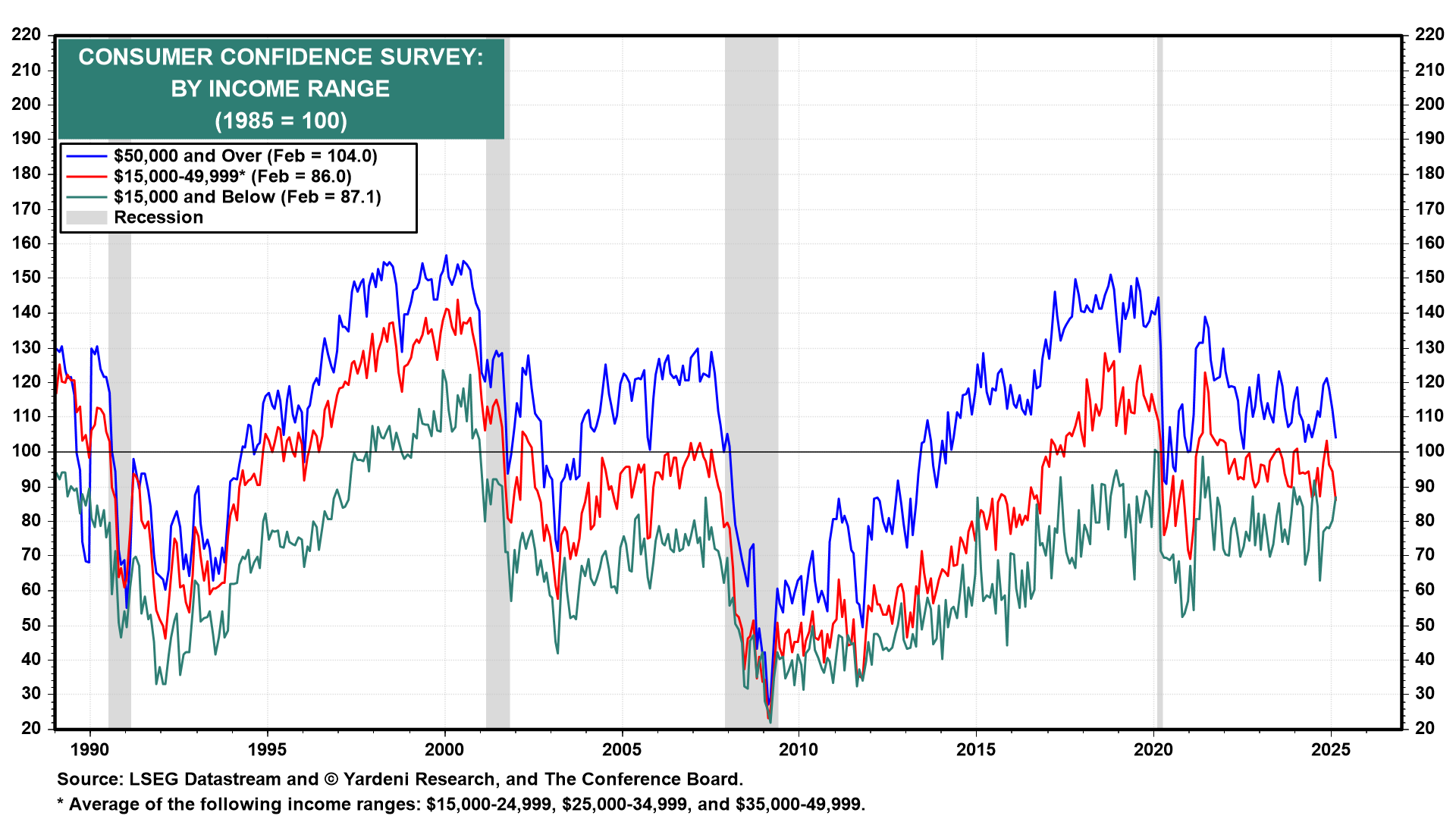

(7) February's decline in the CCI by income ranges was fairly widespread.

(8) The CCI jobs-hard-to-get series confirms the low readings of the unemployment rate and initial unemployment claims.

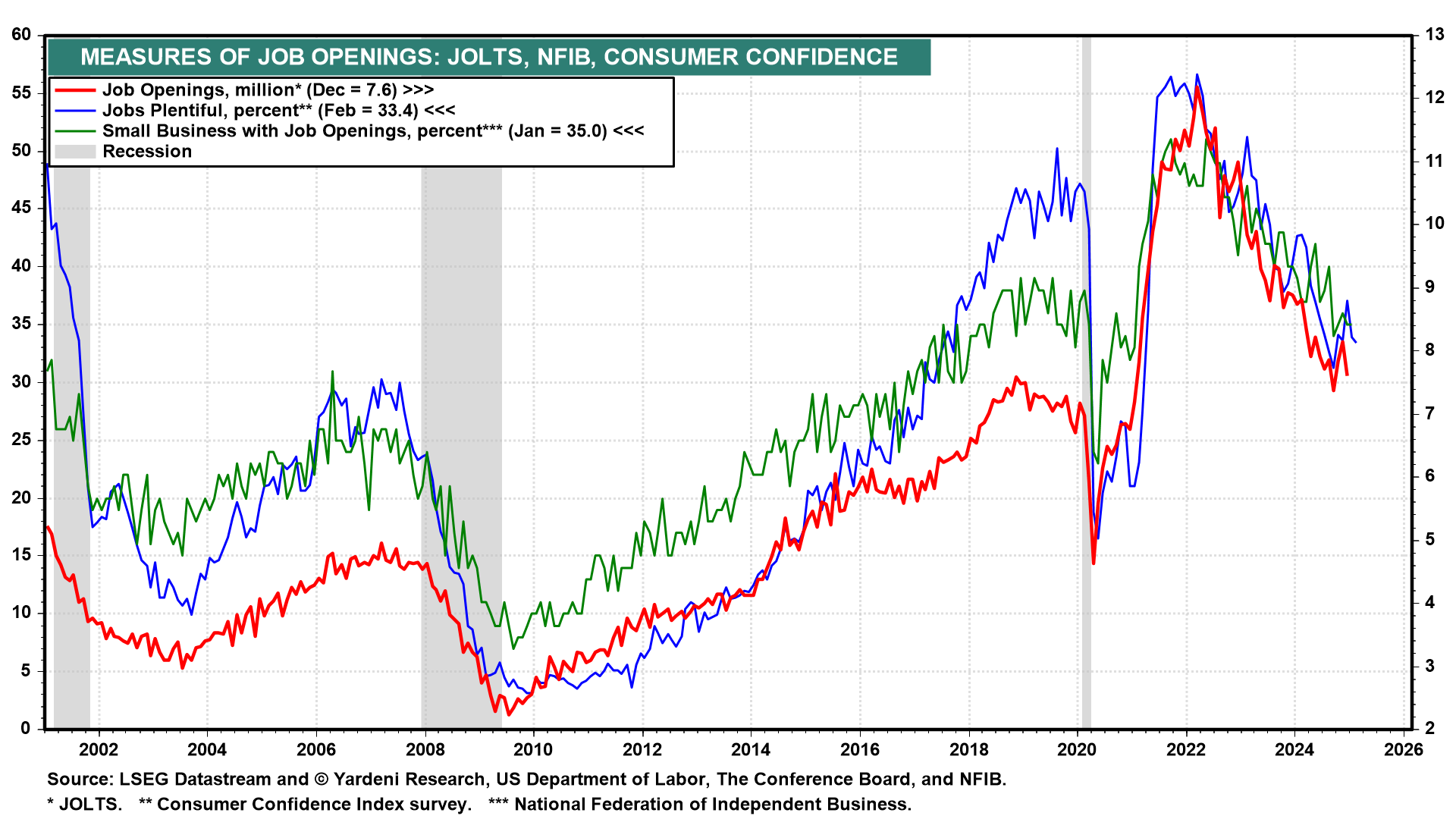

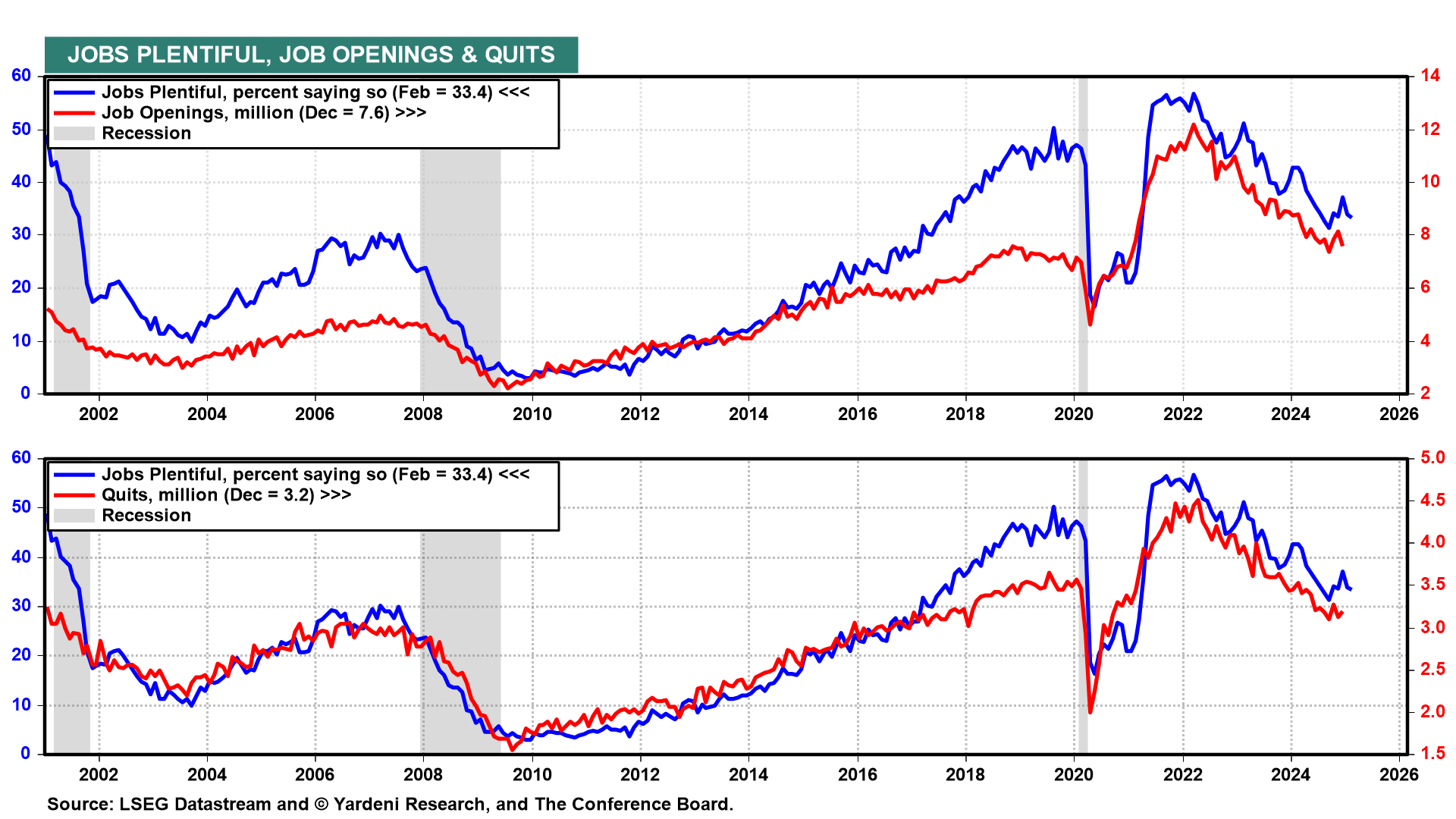

(9) The CCI job-plentiful series confirms that job openings remain relatively plentiful. There has been a decline in this series since the pandemic as fewer people are quitting, so there are fewer positions to fill.

(10) The CCI jobs-plentiful series comes out before the two similar measures of job openings. All together, they show that there are still plenty of job openings. The labor market looks perfectly fine to us. The rebound in the stock market from this morning's selloff suggests that some investors saw a buying opportunity.