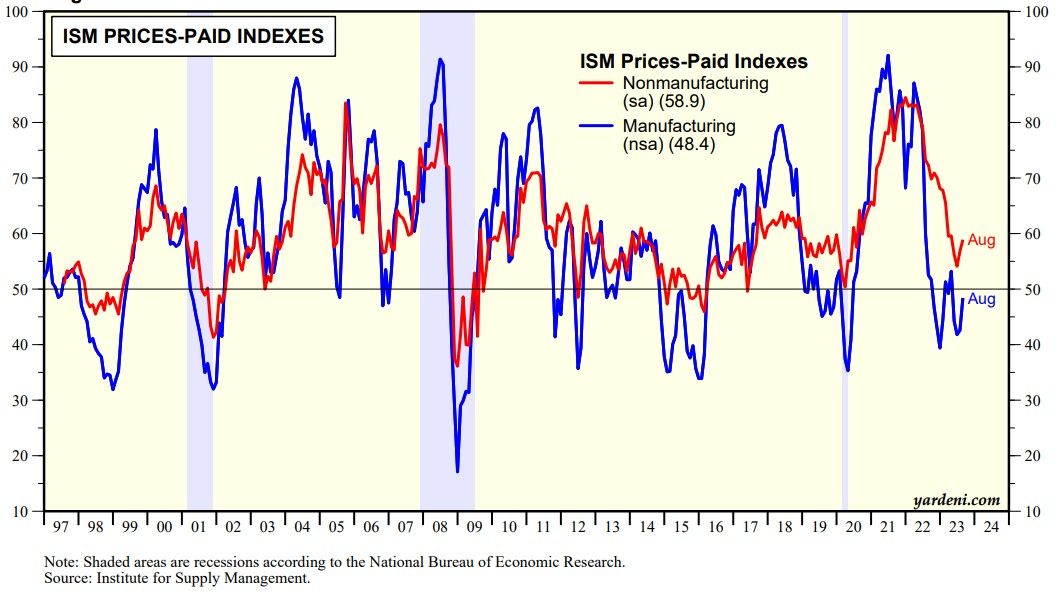

Good news is bad news again. The stock and bond markets sold off yesterday following better-than-expected readings for August's NM-PMI. In addition, the prices-paid indexes for both the NM-PMI and M-PMI increased in August heightening fears that inflation may have stopped moderating (chart). We disagree since both remain well below last summer's peaks.

Today, Q2's revised productivity and costs report showed that hourly compensation rose by 5.7% y/y, while productivity jumped 3.5%. As a result, unit labor costs rose at a modest pace of 2.2% (chart). This series is highly correlated with the CPI inflation rate on a y/y basis and confirms our view that inflationary pressures are easing.

Leer la noticia completa

Regístrese ahora para leer la historia completa y acceder a todas las publicaciones de pago.

Suscríbase a