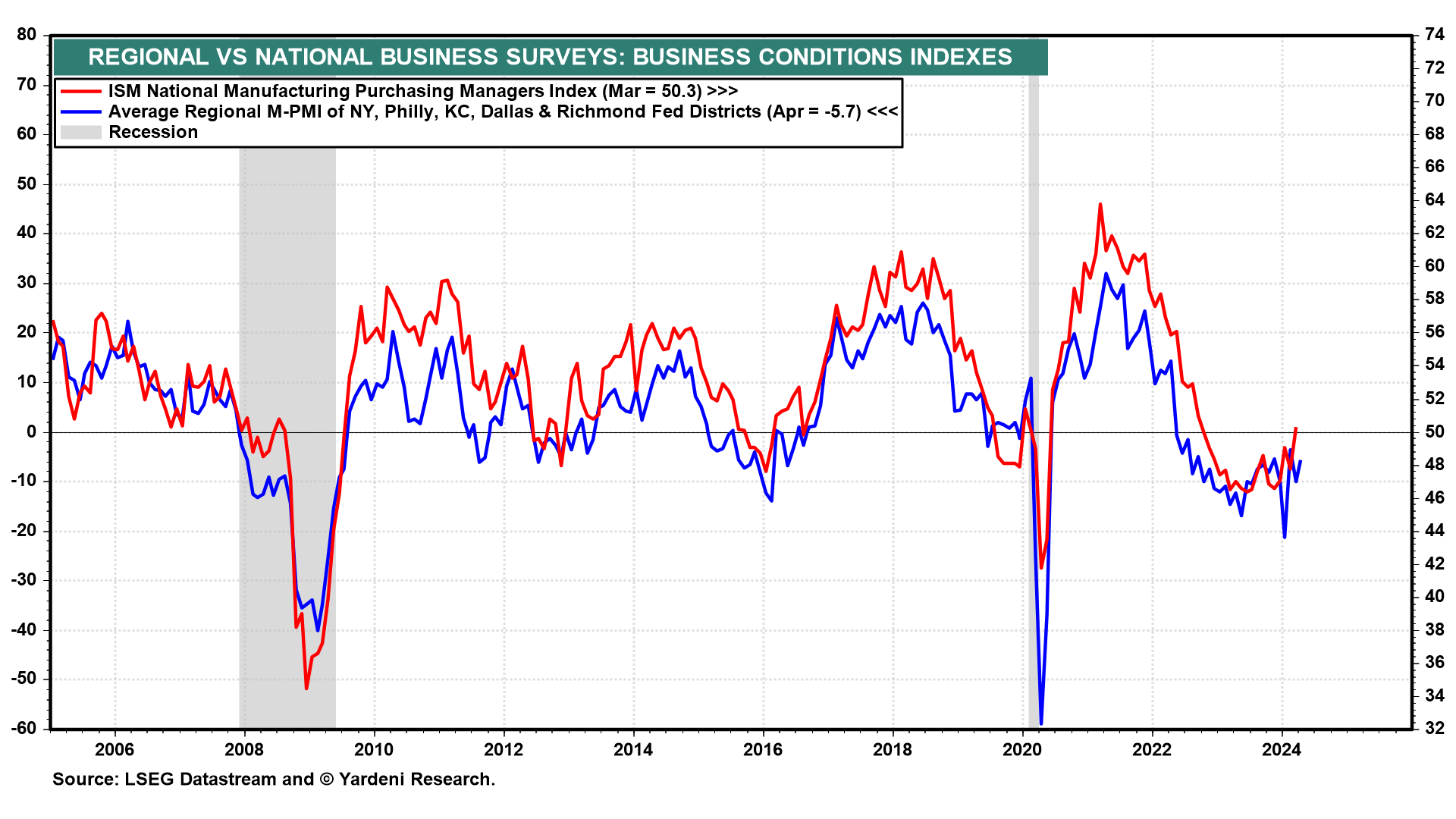

We now have the regional business surveys conducted by five of the Federal Reserve district banks. The average of their general business conditions indexes closely tracks the national manufacturing purchasing managers index (M-PMI), which rose slightly above 50.0 during March following 16 consecutive monthly readings below this level (chart). The regional average index was still negative in April. So it has yet to confirm that the rolling recession in the manufacturing sector is over.

The averages of the regional prices-paid and prices-received indexes have been relatively stable around 20.0 and 10.0, respectively, over the past 12 months or so (chart). These are both relatively normal readings and well below their highs during 2021 and 2022, when pandemic-related supply chain disruptions were most severe. By the way, the PPI final demand inflation rate closely tracks the prices-paid index, which suggests that the former should be around 2.0% y/y. It was 2.1% in March.

Leer la noticia completa

Regístrese ahora para leer la historia completa y acceder a todas las publicaciones de pago.

Suscríbase a