The current issue of Barron’s includes the 2024 S&P 500 targets for six investment strategists including yours truly. Our target is the highest at 5400, based on projected S&P 500 earnings per share of $250 next year. Morgan Stanley’s Mike Wilson has the lowest numbers at 4500 for the index’s price target and $229 for earnings per share. In last year’s survey by Barron’s, we had 4800 as our S&P 500 target for last year with earnings at $225. The low comparable readings were 3930 and $199 for 2023.

Along the way, we trimmed our year-end target to a more reasonable 4600. Then, on June 5, we wrote: “Is all the AI euphoria leading the stock market into another ‘MAMU’—‘Mother of All Meltups’? If so, our 4600 target for the S&P 500 by year-end might prove conservative, not controversial.”

On July 19, we wrote: “The S&P 500 is now almost at 4600. It closed at 4556.27 on Tuesday. Rather than raise our year-end target, we are raising our expectations for what the bull market could deliver through the end of 2024 and beyond. We think that 5400 is achievable by the end of next year. If that happens, then 5800 would be our target for the end of 2025. In other words, we think that the bull market has staying power.”

Last week, we raised our 2025 target for the S&P 500 price index to 6000, as our Roaring 2020s scenario is looking not only possible, but also probable.

Now let’s review our talking points on behalf of the bullish team in the Great Debate. Here’s an even dozen:

(1) Interest rates are back to normal.

Perhaps the Fed hasn’t been tightening monetary policy so much as normalizing it. Interest rates are back to the Old Normal. They are back to where they were before the New Abnormal period between the Great Financial Crisis and the Great Virus Crisis, during which the Fed pegged interest rates near zero.

The normalization theory implies that the Fed might not lower interest rates next year as much as widely expected. That’s because the economy wouldn’t require as much easing to reverse the tightening. If the economy remains resilient but inflation continues to fall closer to the Fed’s 2.0% target next year—both of which we’re expecting—then the Fed might lower the federal funds rate twice next year, by 25bps each time, instead of four times or more as widely anticipated.

(2) Consumers have purchasing power.

Many consumers may soon run out of their excess saving, as the economy’s naysayers are saying. Some consumers could be weighed down by too much consumer debt, especially student loans. Nevertheless, most of them are likely to continue to consume as long as their job security remains high, which it will be as long as there are plenty of job openings and as long as the unemployed and new entrants to the labor force fill those openings. That describes the current state of the labor market.

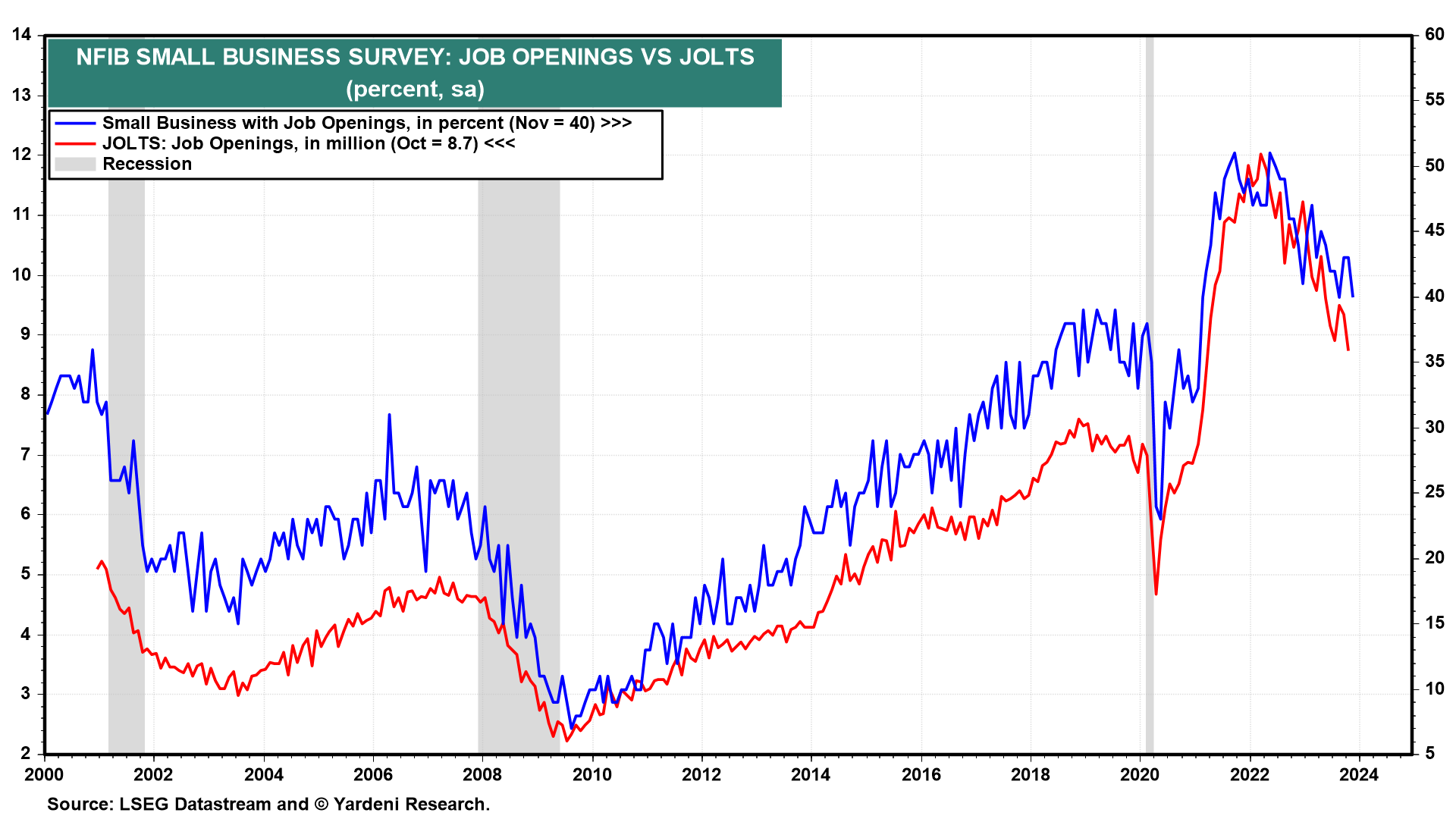

Indeed, during November, 40% of small business owners reported that they have job openings (Fig. 6 below). During October, there were 8.7 million job openings overall in the labor market versus 6.5 million unemployed that month. The labor force has increased 3.3 million during the first 11 months of this year. The household measure of employment is up 2.7 million over the same period.

Pandemic-related excess saving certainly helped to boost consumer spending over the previous three years when unemployment was very high and real wages stagnated. But unemployment is low now (i.e., below 4.0% since February 2022), and real average hourly earnings is rising once again along its 1.4% annualized trendline that started in 1993 (Fig. 7).

Both nominal and real wages & salaries in personal income and unearned personal income (including interest income, dividends, rents, and proprietors’ income) rose to record highs during October (Fig. 8). They probably did so again in November.

(3) Households are wealthy and liquid.

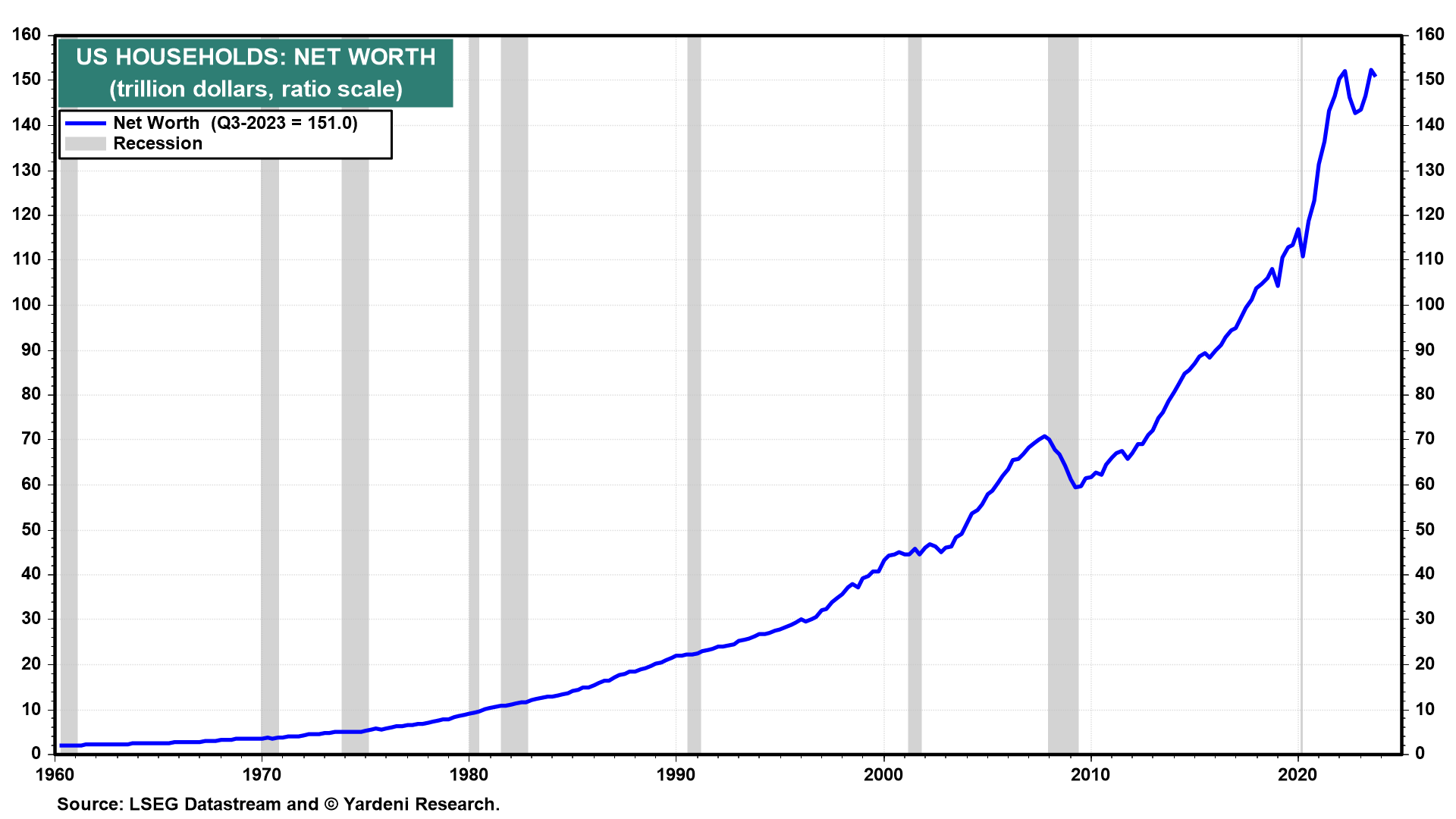

The net worth of American households totaled a staggering record-high $151.0 trillion at the end of Q3-2023 (Fig. 9 below). Their portfolios are diversified in various asset holdings that all are at or near record highs (Fig. 10). There are certainly lots of liquid assets that might be sold to buy stocks and bonds when the Fed decides to lower short-term interest rates. A record $5.9 trillion is in money market mutual funds (MMMF) with a record $2.3 trillion in retail MMMFs (Fig. 11). Commercial bank deposits in M2 totaled $17.3 trillion during the December 12 week (Fig. 12).

There are 86 million households who own their own homes, and 40% of them have no mortgages. Many of these homeowners likely are Baby Boomers. They have mostly followed the advice of Star Trek’s Spock, who often said, “Live long and prosper.” Collectively, the generation held $73.1 trillion of net worth at the end of Q3. Boomers are likely to be among the main beneficiaries of record unearned income streams.

(4) Demand for labor is strong.

From personal experience, we know that some of the Baby Boomers are providing some financial support to their young adult children. The Boomers are also eating at restaurants and traveling more often. They are visiting their health care providers more frequently to make sure that they live long enough to spend some of their retirement nest eggs.

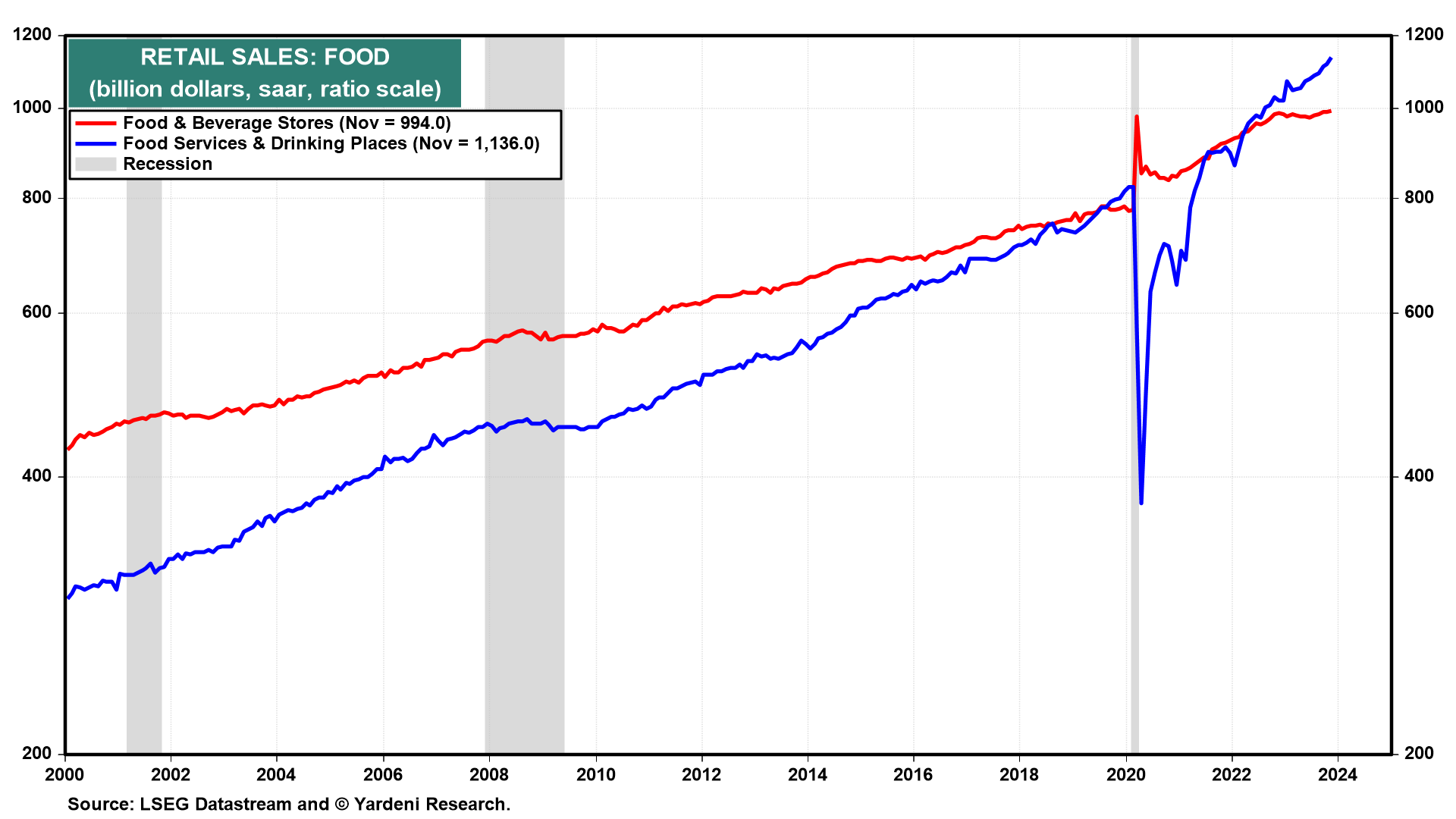

Not surprisingly, November’s better-than-expected retail sales was led by food services, which rose to yet another record high (Fig. 13 below). Employment continues to soar in the leisure & hospitality industry as well as in the health care sector.

(5) Onshoring boom is boosting capital spending.

American and foreign manufacturing companies clearly are onshoring to the US. Supply-chain disruptions during the pandemic and growing geopolitical tensions between the US and China have stimulated the onshoring rush. So has a shortage of workers in China.

The onshoring boom and the federal government’s increased spending on public infrastructure are boosting new orders for construction machinery, which is up 30.5% over the past 24 months through October (Fig. 14). Onshoring and infrastructure investment also explain why construction employment rose to yet another record high of 8.0 million during November despite the recession in single-family housing starts.

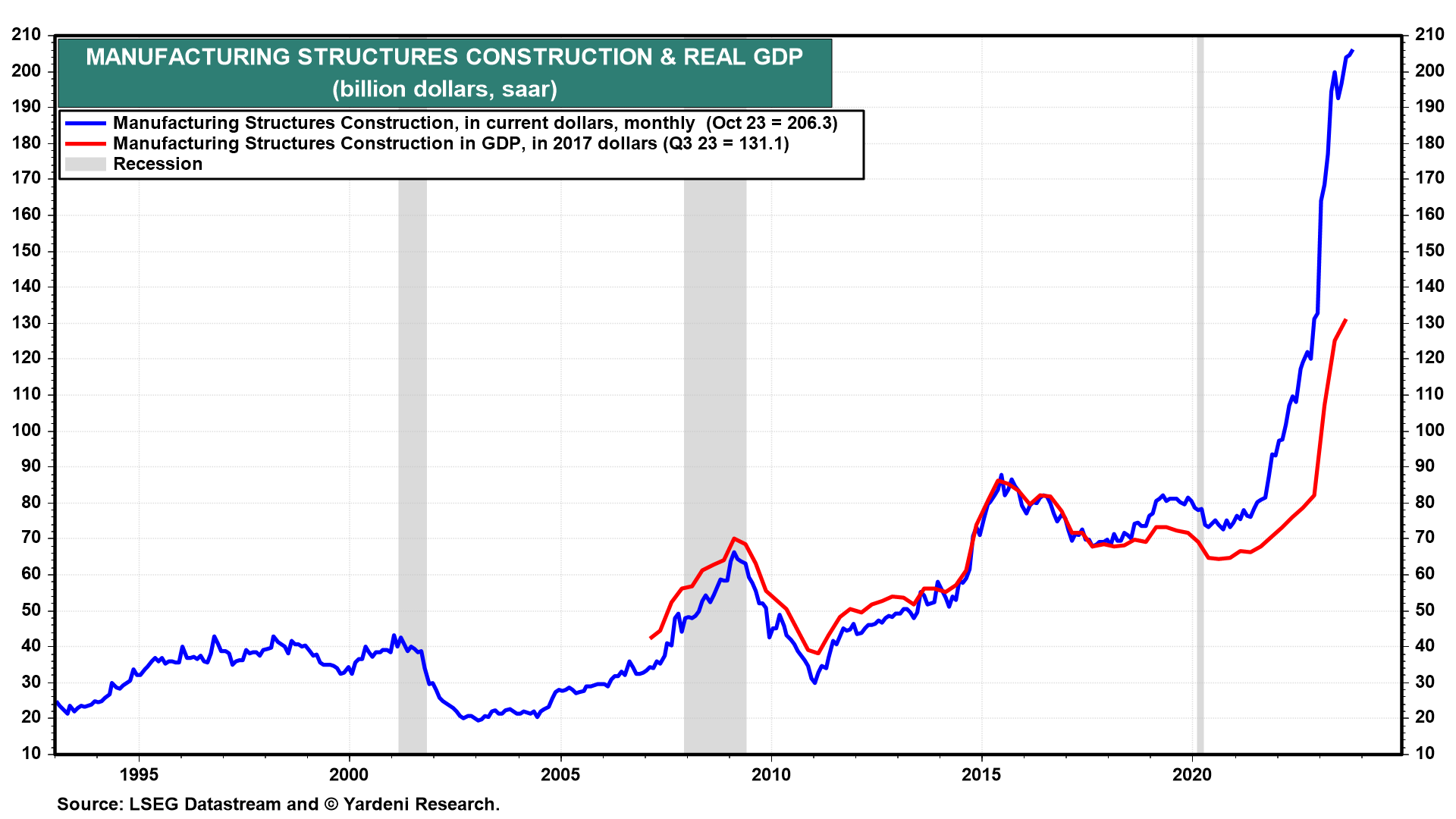

Construction spending on manufacturing facilities is soaring because of the increase in onshoring partly owing to federal incentives. In current dollars, it is up a whopping 71.6% and 136.8% on one-year and two-year bases (Fig. 15 below).

(6) Housing is all set for a recovery.

The plunge in mortgage interest rates since early November undoubtedly will boost new and existing home sales. That should give a boost to housing-related retail sales on appliances, furniture, and furnishings. The rolling recessions in housing and housing-related retailing should turn into rolling recoveries for both.

(7) Corporate cash flow is at a record high.

Leer la noticia completa

Regístrese ahora para leer la historia completa y acceder a todas las publicaciones de pago.

Suscríbase a